Key Points

In May 2026 the CA-TPU index registered 187.46, a 26.1% rebound from April (148.68); its three-month moving average (MA3) rose to 173.21, the 2nd highest of all 209 months since 2009, trailing the June 2020 record (174.09) by just 0.88 points. The current high-pressure episode (MA3 ≥ 150) has now extended into its third month.

Almost the entire rebound came from Uzbekistan, whose sub-index climbed to 472.18 and contributed 81.3% of the composite; meanwhile Kazakhstan, the most heavily weighted country, fell to 40.21, and together with Tajikistan and Kyrgyzstan dragged on the total. The discourse shifted in parallel: risk-, crisis- and sanctions-related terms fell markedly while tariff-, contract- and trade-related terms rose, moving the main thread from “risk framing” toward “concrete trade instruments.”

1. Index Overview

In May 2026 the CA-TPU raw index was 187.46, up 38.78 points (+26.1%) from April (148.68) and up 69.75 points (+59.3%) from a year earlier (117.71). The MA3 reached 173.21, up 15.78 points from April (157.43), remaining above the 150 threshold for a third consecutive month.

Table 1.1 CA-TPU Monthly Comparison

| Indicator | This month (May) | Last month (Apr) | MoM change | Year ago | YoY change |

| CA-TPU raw index | 187.46 | 148.68 | +38.78 (+26.1%) | 117.71 | +69.75 (+59.3%) |

| MA3 (moving avg.) | 173.21 | 157.43 | +15.78 (+10.0%) | 112.58 | +60.63 (+53.9%) |

Source: CA-TPU Index Project, based on the monthly release at catpu.caiees.cn.

In contrast to April, when the raw index fell below the MA3, May saw the raw index rise back above its moving average, restoring a positive gap and signalling a renewed surge in monthly discourse intensity. At 187.46 it is the highest single-month reading since April 2020 (203.34) and exceeds the earlier peak of this episode in March (183.48).

2. Historical Context

Placed among the 209 months since 2009, the May MA3 of 173.21 ranks 2nd in the entire history, only 0.88 points below the June 2020 record (174.09); the raw index of 187.46 ranks around 8th. The most striking historical feature this month is that the MA3 has approached the all-time high.

Table 2.1 MA3 All-Time Top 6

| Rank | Month | Raw index | MA3 | Context |

| 1 | 2020-06 | 169.02 | 174.09 | COVID-19 pandemic |

| 2 | 2026-05 | 187.46 | 173.21 | Current (tariff war) |

| 3 | 2026-03 | 183.48 | 166.34 | Current (tariff war) |

| 4 | 2012-09 | 249.81 | 161.40 | Single-month spike |

| 5 | 2020-05 | 149.90 | 158.32 | COVID-19 pandemic |

| 6 | 2026-04 | 148.68 | 157.43 | Current (tariff war) |

Source: CA-TPU Index Project.

Among the six highest MA3 readings in history, the current tariff-war episode already occupies three (May, March, April), tying the early-COVID period of 2020 as the two most concentrated high-pressure stretches since the index began. The high-pressure state (MA3 ≥ 150) has lasted three months, matching the duration of the early-COVID episode.

3. Shift in Discourse Structure

The project team tallied, after case-form lemmatisation, the keywords in all “high-value news” in May (articles that simultaneously hit the trade, policy and uncertainty categories) and compared them with April. The discourse structure shifted markedly.

The rising lemma families were concentrated in concrete trade instruments: contracts/treaties (договор) up 32.9%, tariffs (тариф) up 25.8% and trade (торговля) up 16.8%. The falling families clustered in risk and bargaining language: uncertainty (неопределенность) down 57.5%, sanctions (санкции) down 39.3%, policy (политика) down 35.7%, risk (риск) down 30.7% and crisis (кризис) down 28.4%.

Table 3.1 Keyword family MoM change (May vs Apr, lemmatised)

| Category | Lemma family | May | Apr | MoM |

| T | договор (contracts/treaties) | 101 | 76 | +32.9% |

| T | тариф (tariffs) | 78 | 62 | +25.8% |

| P | министерство (ministries) | 159 | 135 | +17.8% |

| T | торговля (trade) | 438 | 375 | +16.8% |

| T | санкции (sanctions) | 128 | 211 | -39.3% |

| P | политика (policy) | 144 | 224 | -35.7% |

| U | риск (risk) | 305 | 440 | -30.7% |

| U | кризис (crisis) | 96 | 134 | -28.4% |

| U | неопределенность (uncertainty) | 17 | 40 | -57.5% |

Source: CA-TPU Index Project; frequencies from four-country high-value news, after lemmatisation.

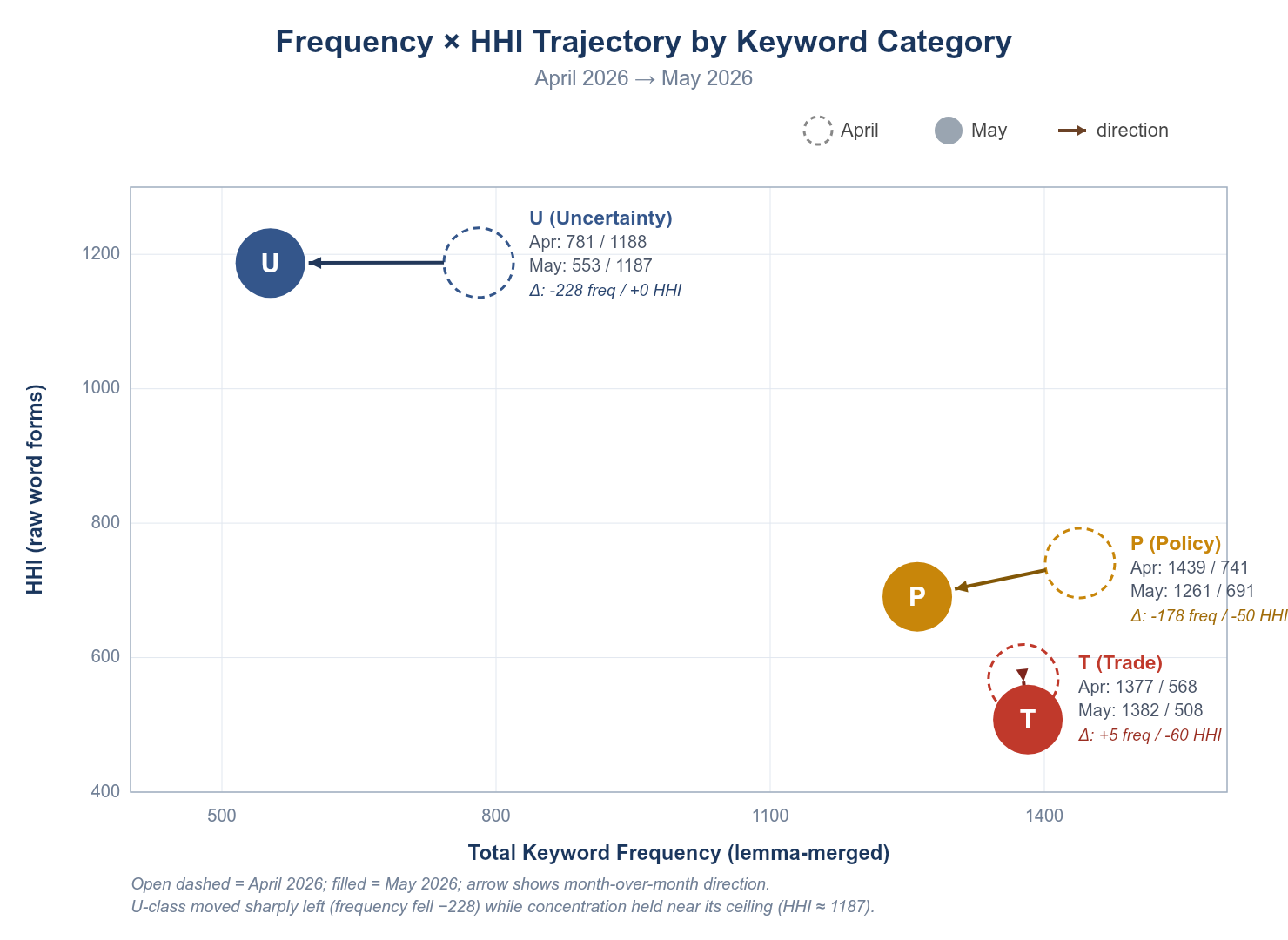

The topic-concentration (HHI) of the three categories diverged: trade and policy eased from April (trade 567.8 → 507.7, policy 740.7 → 690.5), indicating these topics became more dispersed in May; uncertainty stayed high (1187.6 → 1187.1), still tightly concentrated on the single “risk” family.

Figure 3.1 Keyword frequency × topic concentration (HHI) trajectory: April → May 2026

The trajectory shows the uncertainty category (U) moving sharply left in volume (frequency 781 → 553) while barely changing vertically — discourse “shrank” yet stayed “tightly focused”; the trade category (T) held roughly flat in volume while its concentration fell, meaning trade topics stayed prominent but became more dispersed and concrete.

4. Country Divergence

The CA-TPU index composites four national sub-indices by trade weight (KZ Kazakhstan, UZ Uzbekistan, KG Kyrgyzstan, TJ Tajikistan). In May the divergence among the four reached its widest in recent months.

Table 4.1 Four-country sub-index trends

| Country | May | Apr | MoM | Year ago |

| Kazakhstan | 40.21 | 49.84 | -19.3% | 101.45 |

| Uzbekistan | 472.18 | 330.72 | +42.8% | 177.89 |

| Kyrgyzstan | 93.35 | 97.94 | -4.7% | 51.75 |

| Tajikistan | 146.34 | 171.31 | -14.6% | 98.67 |

Source: CA-TPU Index Project. CA-TPU is a trade-weighted composite of the four countries; weights are based on 2024 trade data, with Kazakhstan around 60% and Uzbekistan around one-third.

Weighted, Uzbekistan alone contributed about 81.3% (≈152.4 points) of the May composite — the dominant driver — while Kazakhstan, despite the highest trade weight (around 60%), contributed only about 12.3%. Put differently, of the 38.78-point net increase from April, Uzbekistan alone added about 45.7 points while the other three together subtracted about 6.9 — the month’s rise was entirely Uzbekistan-driven.

It should be noted that Uzbekistan’s absolute sub-index level is systematically inflated by sparse base-period samples (see Section 6); its directional change can be read normally, but its absolute magnitude should not be over-interpreted.

Table 4.2 Four-country distribution of major keyword families (May, lemmatised)

| Cat. | Lemma family | Total | KZ | UZ | KG | TJ |

| P | решение (decisions) | 296 | 79 | 157 | 40 | 20 |

| T | торговля (trade) | 438 | 118 | 201 | 74 | 45 |

| T | соглашение (agreement) | 267 | 44 | 169 | 37 | 17 |

| T | экспорт (exports) | 221 | 103 | 85 | 21 | 12 |

| U | риск (risk) | 305 | 135 | 78 | 68 | 24 |

| T | санкции (sanctions) | 128 | 13 | 73 | 41 | 1 |

| T | договор (contracts/treaties) | 101 | 27 | 29 | 38 | 7 |

| T | тариф (tariffs) | 78 | 26 | 16 | 30 | 6 |

Source: CA-TPU Index Project; frequencies from four-country high-value news, after lemmatisation.

By country, Uzbekistan’s discourse centred on “agreement, decisions, trade” — of the 267 mentions of the “agreement” family, 169 (63.3%) came from Uzbekistan, continuing its “active negotiation” profile. Kazakhstan was dominated by “risk” and “exports”: of the 305 mentions of “risk,” Kazakhstan alone accounted for 135, and of the 221 mentions of “exports,” 103 — reflecting the largest economy’s high sensitivity to tariff pass-through.

Kyrgyzstan showed the highest relative concentration in “sanctions” (41) and “tariffs” (30), consistent with its role in re-export trade and its sensitivity to secondary sanctions; Tajikistan’s small sample base keeps its absolute frequencies low, limiting their interpretive value.

5. Outlook and Variables to Watch

Drawing the month’s data together, the following variables are worth tracking through June–July.

First, whether Uzbekistan’s sub-index can hold its high. At 472.18 this month it is an extreme reading historically; it may reflect genuinely intense negotiation and policy activity, or carry a base-period amplification. A clear pullback in June would mean May’s surge should be read as a single pulse rather than an established trend.

Second, whether concrete trade-instrument families such as “tariffs” and “contracts” can sustain their rise. Continued gains would mean discourse is moving from “risk framing” to “substantive arrangements,” with concrete outcomes possibly emerging in June–July.

Third, whether Kazakhstan’s sub-index stops falling and rebounds. The country has declined for several months, and this month’s 40.21 is a recent low, diverging from the regional surge; a sudden upturn there would be a broader-based risk signal.

Fourth, whether the MA3 can break the June 2020 record (174.09). At 173.21 it is one step away; if the raw index stays above 150 in June, the MA3 will set an all-time high, confirming the severity of the current episode.

6. Accompanying Materials

This report is accompanied by two items. The first is the data-transparency package, containing the month-level aggregated data underlying every chart in this report (10 CSV files) and a bilingual data-usage guide, to allow independent verification by third parties. The second is a plain-language brief for businesses and trade practitioners, interpreting the month’s key points and their implications for business practice in non-technical language. The key figures in both are fully consistent with this report.

On Uzbekistan’s absolute sub-index level: since January 2026 the country’s readings have run persistently high, related to its sample characteristics within the 2015–2019 base period; this is a methodological limitation the project team has identified. For this sub-index, attention should focus on direction and relative trend rather than absolute level. This caveat is kept consistent across the three language editions and the data package.

About the CA-TPU Index

The CA-TPU (Central Asia Trade Policy Uncertainty Index) was developed by the team of Professor Zhang Lijie at the School of Economics and Management, Xinjiang University, built on the economic-policy-uncertainty approach of Baker, Bloom and Davis (2016), covering the main Russian-language media of Kazakhstan, Uzbekistan, Kyrgyzstan and Tajikistan. The index measures the intensity with which these countries’ mainstream media simultaneously discuss trade, policy and uncertainty; the base period is 2015–2019, normalised to a base-period mean of 100, and it is released monthly. Full methodology, historical data and trilingual reports are available at catpu.caiees.cn.

This report is a non-profit academic output, independently funded, and does not constitute investment advice or a basis for business decisions. Attribution: CA-TPU Index Project.